Over the past decade, we have witnessed the rapid evolution of China’s consumer infrastructure. Each shift in channels has given rise to a new generation of consumer champions.

However, as the shelf-driven dividends of “products gathering by category” gradually fade and the market enters a new stage of “people grouping by affinity,” returning to the essence of the consumer and re-understanding demand has become an essential discipline for every practitioner.

Recently, Robert Chang, Founding Partner of GenBridge Capital, joined the podcast Gentle & Sharp 温柔一刀 for an in-depth conversation.

As a consumer investor with two decades of experience in the field, he traced the three generational shifts in Chinese consumption over the past 20 years and proposed that the more important question for consumer investing going forward should be: what value does a brand truly create for consumers?

It was also a moment of personal candor from an investor.

In the episode, Robert also shared his reflections on China’s consumer industry from the perspective of a “small-town exam taker” who came from Alxa, Inner Mongolia. As cycles turn and involution intensifies, “scaling up” is no longer the only remedy. Investors and entrepreneurs alike are rediscovering their own agency. This has made us believe all the more firmly that:

The ultimate meaning of consumer investing lies far beyond the mere pursuit of victory.

Whether it is enabling people to enjoy a bowl of steaming, high-quality rice, own a comfortable piece of solid-wood furniture, or fill a bag with affordable snacks after work without pressure, we hope to see the many ordinary consumers who live earnestly while carefully managing their daily budgets.

With solid, high-quality products, we hope to carry the small joys of everyday life. This is not only the original intention behind GenBridge’s consumer investing, but also the warmest foundation that enables great businesses to endure across cycles.

Below is an edited excerpt from Robert’s remarks on the program.

Two decades of consumer evolution through the lens of snacks

I was born in Alxa, Inner Mongolia, one of the most remote places in the region. Alxa is larger than Zhejiang Province in land area, yet has a population of fewer than 300,000. Several of China’s largest deserts are located there.

Growing up in such a far-flung place, distant from the centers of power and attention, I was, in many ways, a typical “small-town test-taker.”

Many years later, after I became a consumer investor, I often felt that Alxa was like a nerve ending of Chinese consumption. For a long time, the new business models we discussed in major cities seemed to have little to do with the relatives who remained there. My family knew that I worked in investment, but whenever I mentioned the brands we had invested in, their faces would always show a look of confusion.

It was only in recent years that this suddenly began to change. In my hometown, Mixue, Guoquan, Luckin Coffee, and even CHAGEE have opened stores. My uncle, now in his seventies, can even skillfully search for recipes on social platforms and cook lunch for his grandson.

In 2024, Alxa’s first McDonald’s opened. Source: Alxa Media

After 20 years in consumer investing, my deepest realization is that consumption is constantly evolving, and “new consumption” is happening every day. The new consumption of each era is defined in relation to the infrastructure and consumer groups of that particular time.

If we were to make this trajectory more tangible, the snack category would be one of the most vivid time machines.

When I first entered the industry 20 years ago, people believed that snacks represented a vast market opportunity. Back then, if you went to RT-Mart, the shelves were stocked with brands such as Aming Guazi and Hua Wei Heng.

Later, Laiyifen appeared on the streets of Shanghai, while Bestore emerged in Wuhan. These were the leading “new consumption” brands of that era. They carefully selected snacks from wholesale markets, packaged them, and placed their own logos on them. Consumers perceived the quality to be high, and these companies were also able to generate solid profits, with gross margins of around 50%. This was a snapshot of the specialty-store era in China’s snack industry.

But the story was far from over. By 2013, online infrastructure had begun to explode, and Three Squirrels emerged. In its first year, the company generated RMB 30 million in sales; in its second year, it surpassed RMB 100 million; by 2019, it had reached RMB 10 billion in scale. When I visited their factory, I saw them using sieves to sort macadamia nuts. The smaller ones would fall through directly, while only the largest and best-quality nuts were kept and sold online.

Why be so stringent? Because the e-commerce era created direct interaction with consumers. If a product was not good enough, consumers would leave negative reviews immediately. This sense of reverence toward direct consumer feedback forced quality to improve.

Just as people began to believe that online channels were the endgame, Snack Is Busy appeared on the streets of Changsha in 2019. There, a bottle of Nongfu Spring sold for only RMB 1.2, and products across the store were priced at 30% to 40% discounts. Through extreme gains in efficiency, the company could add only a 30% gross margin and still allow both franchisees and the company itself to make money.

And this is still not the endpoint. Today, Xueji Snacks and Luxihe have entered shopping malls, with bright, clean storefronts, open-shelf displays, and on-site baking. Consumers can taste before they buy.

Over the past 20 years, snacks have evolved from supermarket shelves to branded specialty stores, from direct-to-consumer online channels to offline stores defined by extreme efficiency and on-site experience. Behind this transformation is the continuous renewal and extension of China’s commercial infrastructure, as well as the gradual elevation and diversification of consumer demand.

In this process, the new business formats that once felt distant and unreachable have gradually reached the deepest nerve endings of this vast land, connecting consumers who live in different cities and lead different lives

Recognizing real mass-market demand

For a long time, many business discussions centered on how to drive consumption upgrades and encourage people to buy more expensive products. The needs of ordinary mass-market consumers were often vague, and there was even a lack of a dedicated commercial ecosystem designed to serve them.

On this issue, I once learned a profound lesson: Pinduoduo. Around ten years ago, when it emerged with its “RMB 9.9 with free shipping” model, we discussed it internally and saw it as nothing more than a business for consumers beyond Beijing’s Fifth Ring Road. When it described itself at the time of its listing as “Costco + Disney,” it felt even harder to understand.

But looking back several years later, we had indeed misunderstood it.

Pinduoduo not only identified the most cost-effective products within each price band; more importantly, it reduced the pressure people felt when making purchasing decisions. Through one RMB 9.9 purchase after another, consumers gained real, tangible joy. The ability to attach emotional value to basic consumption is truly remarkable.

At the beginning of this year, Busy Ming Group, formed through the merger of Snack Is Busy and Zhaoyiming Snacks, successfully listed in Hong Kong. From emerging to exploding in scale, snack discount retailers created a commercial miracle worth hundreds of billions of RMB in just a few short years. Their rise follows the same logic.

When people first see one of these stores, their instinctive reaction may be: isn’t this just an ordinary discount store? Isn’t it simply selling things a little cheaper? In fact, it is not.

Mr. Yan Zhou, the Founder, once made it clear that their original intention was to help consumers access, afford, and enjoy good products, with the goal of becoming “the people’s snack brand.” In a 100-square-meter store, 2,000 products are densely displayed. Many items can be purchased individually, costing only RMB 1 to 3 each, allowing consumers to fill their shopping baskets without any pressure. At checkout, more than a dozen items may add up to just over RMB 20.

In the first half of this year, Mingming Henmang also opened a “Snack Kingdom” in Changsha. Certified by Guinness as the world’s largest snack store, it spans more than 13,000 square meters. Inside are giant snack models, snack tunnels, and all kinds of novel flavors that consumers may have never seen before. It is fun, yet not expensive.

At the moment of checkout, consumers experience the joy of “snack freedom.” Together with clean and orderly stores and endorsements by major celebrities, this makes shopping there feel both dignified and enjoyable.

Whether it is value-for-money e-commerce platforms, snack discount retailers, or Mixue stores found in every corner of the country, what they are doing is, at its core, providing highly cost-effective basic products while attaching emotional value to them—allowing the most mainstream mass-market consumers to be truly seen and respected.

The reconfiguration of value in consumer goods

Over the past decade, and even longer, Chinese consumption went through a period of rapid acceleration. The core logic of that era was what we may call “products clustering by category.”

What we mean by “products clustering by category” is, in essence, an efficiency-driven expansion centered on goods. As long as the supply chain was strong enough and the right categories were selected, companies could ride the dividends of ever-upgrading e-commerce or offline channels, quickly seize territory, and scale up. Markets were divided by category, and what everyone pursued was victory in industry structure and business model.

At that time, we often looked up to multinational giants and wondered why China did not have large-scale quick-service restaurant chains, or why it did not have globalized tea beverage brands. Later, with the dividends of e-commerce and offline channels, we filled these gaps, and many companies reached RMB 5 billion, or even over RMB 10 billion, in scale.

But once everyone had achieved the scale they wanted, a new question emerged: how do you build strength? Why does scale not necessarily translate into profit?

For example, some companies generate more than RMB 10 billion in annual sales, yet end up with only RMB 50 million in profit, while over RMB 1 billion is paid to channels. People suddenly realized that victory based purely on business model and industrial efficiency was no longer enough.

Profit can only come from two places: either from defeating competitors in brutal hand-to-hand combat, or from earning a premium through consumers’ recognition and affection.

Today, we have entered a new stage of “people clustering by affinity.”

The difference between the two is that “products clustering by category” is a supply-side mindset, focused on filling shelves with good products. “People clustering by affinity,” by contrast, is a demand-side mindset. Brands must become fully consumer-centric, identify groups of people with specific emotions and lifestyles, and respond to their deeper needs.

In today’s world of extreme product abundance, consumer value is ultimately a combination of several things: performance, meaning whether the product is good; price, meaning whether it is worth it; convenience, meaning whether it is delivered fast enough; and emotion, meaning whether I love it.

Under today’s highly developed commercial infrastructure, price and convenience have already become the baseline requirements. What truly tests a founder’s capability is how to align functional value with emotional value.

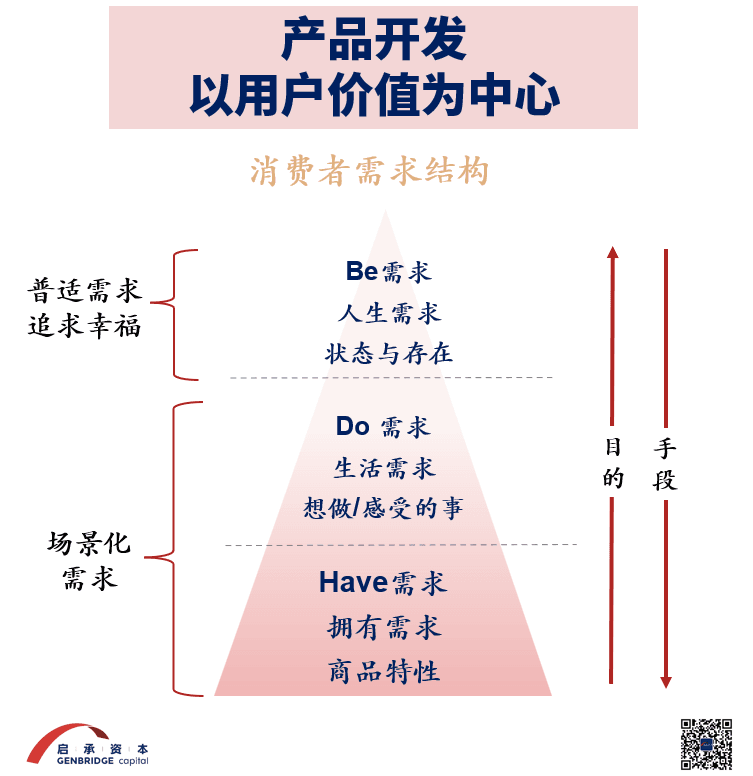

There is a very concise model for brand upgrading: HAVE, DO, BE. HAVE represents the basic function of a product; DO represents what task the product helps consumers solve in a specific scenario; and the highest level, BE, is the core of the brand—it shapes what kind of person consumers feel they are becoming.

The century-old luxury houses of France and Italy are built around aristocratic stories and class symbols from the past. In China today, we are also building our own “BE.”

For example, one emerging domestic bag brand in the market is not merely a functional tote for carrying a laptop. It tells consumers a story of Shanxi—the Yellow River, pebbles, and the eaves of ancient architecture—offering an aesthetic identity and sense of belonging rooted in Chinese culture. When consumers choose it, they are in fact completing a connection with the self.

Over the next 20 years, Chinese brands no longer need to become China’s answer to anyone else. With world-class supply chains and product capabilities already in place, the next frontier is not imitation, but meaning—placing consumers at the center and creating brands that speak to who they are and who they aspire to become.

What we ultimately need to do is enable the broad base of consumers, when using these products, to feel comfortable and reassured in their everyday lives, and, almost imperceptibly, to connect with a better version of themselves. This is the most enduring beauty of consumer investing and brand building.

Seeking more enduring meaning beyond the desire to win

As an exam-taker who came from a small town, I used to believe that winning was what mattered most. In order to get things done, people often push efficiency to the extreme, driving not only themselves to the brink, but also everyone around them.

But when you truly win in the battlefield of business, achieving scale and market value, you gradually come to realize that you do not actually like that tightly wound version of yourself, nor do you like relationships that feel so cold.

Over the past few years, I have gradually learned to become more aware of myself and of others. When facing founders and partners, I have also begun to ask myself: can I stand there, truly see what is in their hearts, understand their emotions, and accompany them in overcoming difficulties? If we shift to another dimension and turn competition into mutual support in pursuit of something meaningful, I have found that the journey we walk together is already a source of profound happiness in itself.

This has also been my greatest awakening over the past two years: when we are winning for the sake of winning, have we truly seen the users behind it all?

Today, after doing so many things and investing in so many companies, everything ultimately comes down to one thing: that this generation of Chinese consumers, after using your product, can at least feel comfortable and reassured in their everyday lives, and further feel a connection with a “better version of themselves.” That, to me, is something profoundly beautiful.

The ultimate meaning of consumer investing lies far beyond the simple desire to win. When we set aside our obsessions with winning, losing, and scale, return to real, specific individuals, and help bring about this beautiful connection, I say to myself:

Thankfully, the truest thing has always remained.