Over the past few years, has China experienced consumption upgrading or downgrading?

Different people offer different answers. Many believe it is consumption downgrading, as consumers have become more budget-conscious and many products are cheaper than before.

However, we observe a clear and definitive trend: the consumer sector is undergoing an “upgrade without price increases.”

This may sound counterintuitive. The immediate reaction is often: if consumption upgrades without price increases, wouldn’t that imply losses? In fact, it does not.

In recent years, the consumer market has faced significant headwinds. Yet since the second half of last year, signs of recovery have emerged, with a number of companies rebounding and actively pursuing IPOs. In just the past six months, I have attended two listing ceremonies at the Hong Kong Stock Exchange, and three additional portfolio companies have submitted listing applications.

In this new cycle, many brands are upgrading products while maintaining affordable pricing. Rather than incurring losses, they have improved end-to-end efficiency through business model innovation, reducing costs and achieving steady growth.

In essence, “upgrade without price increases” means recognizing consumers’ aspirations for a better life and meeting those needs through more efficient business models.

This article is adapted from a talk by Robert Chang, Founder of GenBridge Capital, at Hundun Academy. He reviews the evolution of the consumer sector and, through selected case studies, outlines new approaches for brands under the paradigm of “upgrade without price increases.” It encapsulates his two decades of entrepreneurial and investment experience in consumer industries, with the aim of offering meaningful insights to practitioners in the field.

Perspective: We are entering an era where consumers decide

Looking back, the consumer market has undergone a shift in momentum; at its core, this reflects an evolution in the fundamental logic of consumption in China—

Era 1.0: Production determines consumption

Early brands focused on developing products that met the broadest common demand, leveraging television media and striking advertising to attract distributors and achieve nationwide distribution, ultimately becoming household names.

It was an era driven by factories and brands, where the core competitive advantage was “finding good products and making them accessible to consumers.”

Era 2.0: Channels determine consumption

From the 1990s onward, international retail chains such as Walmart and Carrefour entered China, drawing massive crowds, while domestic players like Suning and Gome rose rapidly, driving a boom in appliance consumption. Modern retail chains reshaped the consumption landscape.

After 2010, online channels in China surged. From the all-encompassing Taobao and premium-focused Tmall to next-day delivery from JD.com, followed by ultra-low prices on Pinduoduo, livestream commerce on Douyin, and 30-minute delivery from Meituan—many new brands rose rapidly on the back of channel tailwinds.

In just a few decades, China’s consumer market has traversed a path that took Western economies over a century. Today, with abundant products and channels, the market has shifted from seller-driven to buyer-driven, entering an Era 3.0 where consumers are in control.

As Jeff Bezos noted, one should focus on what does not change. In consumer demand, several fundamentals remain constant: quality, value for money, convenience—and increasingly, emotional satisfaction.

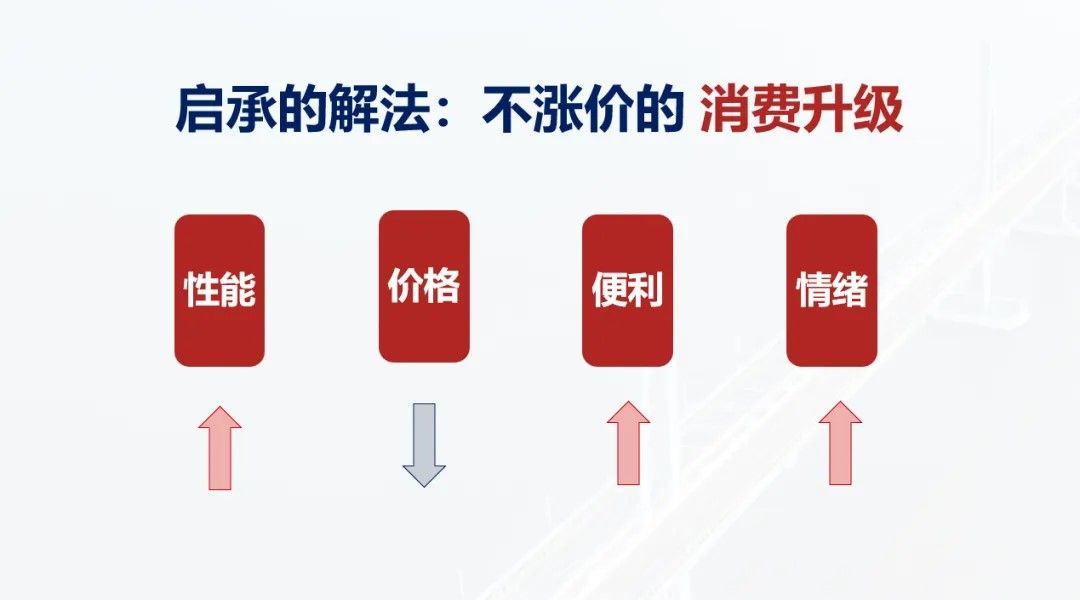

Accordingly, a clear and enduring consumer value equation can be summarized as: performance + price + convenience + emotion

With this framework, several consumption trends become easier to understand:

1) K-shaped channel divergence: consumers are willing to travel to Sam’s Club, Hema, and Pangdonglai for higher-quality products and unique experiences, while also purchasing lower-priced goods from discount retailers such as Aldi, Hema NB, and Busy Snacks. Online, a similar pattern emerges: users turn to Xiaohongshu and Douyin for quality, and to Pinduoduo for value. This is a classic “K-shaped” divergence.

2) Brand emergence and iteration: where Starbucks once dominated, shopping malls now host M Stand and Peet’s, while office districts feature Manner and Luckin. In sportswear, Nike and Adidas no longer dominate exclusively, as new brands emerge across niche segments. Many once-familiar brands are now seen by younger consumers as outdated, while new entrants are rapidly gaining prominence.

Underlying these shifts is a fundamental change: consumers now hold true decision-making power. Through their choices, they are reshaping product offerings, channels, and brand landscapes. The gears have begun to turn—ushering in a new era of consumption.

Approach: Upgrading without price increases

As discussed, consumer demand in China has evolved. Many entrepreneurs ask: what are the new solutions?

Starting from the consumer value equation (performance + price + convenience + emotion), we can derive four levers: improving performance, lowering price, enhancing convenience, and elevating emotional value. These elements can be flexibly combined.

Let us illustrate with two portfolio case studies.

Solution 1: Higher performance, lower price

In recent years, many Chinese entrepreneurs have explored a simple idea: as consumer demand upgrades, adopting superior business models—particularly those rooted in e-commerce—and shortening supply chains can reduce prices and create stronger competitiveness. This is “higher performance, lower price.”

If one sector has faced exceptional difficulty in recent years, it would likely be real estate. Yet surprisingly, despite consecutive declines in residential property sales, a furniture brand we invested in has achieved 50% annual growth for several years, expanding from RMB 1 billion to RMB 15 billion in five years and emerging as a dark horse in China’s furniture industry.

This brand is Yeswood.

In China, most consumers traditionally purchased engineered wood furniture, either from IKEA or furniture malls. However, households with children or elderly members often become concerned about formaldehyde emissions, leading many to shift toward solid wood furniture.

Yeswood seized this opportunity and began selling solid wood furniture online. Initially, we were curious: who would purchase large items such as beds and bookshelves online? We called many users to understand why they chose this channel.

The answer was simple: Yeswood delivered products that were both high-quality and affordable.

A 1.8-meter solid wood bed sold for just RMB 1,000—comparable to IKEA’s engineered wood alternatives. Beds of similar quality could cost several thousand RMB in traditional furniture stores, leading many consumers to initially doubt their authenticity. Only after purchase and installation did they realize the product was indeed high-quality solid wood, complemented by thoughtful features such as wireless charging and automatic night lighting.

How did Yeswood achieve this?

In the traditional offline model, furniture brands rely on multiple layers of regional distributors, with cycles measured in years. From factory to end consumer, markups can reach 5–10x. In contrast, the online model enables production upon order and direct delivery to the customer, significantly shortening cycles and reducing markups to around 1.5x—while still maintaining healthy margins.

Subsequently, to meet consumers’ desire to see and experience products firsthand, Yeswood expanded into furniture malls and shopping centers. It also collaborated with film and television productions to create relaxed, home-like settings in visual content.

As a result, consumers began to think: while upgrading to a new home may be difficult, upgrading to better furniture is attainable. This has become a natural choice for younger consumers.

Yeswood firmly delivered higher performance (upgrading from engineered to solid wood) while lowering prices (reducing markups from 5–10x to 1.5–2x), and gradually built emotional value around “a greener home.” This is a quintessential example of upgrading without price increases.

Solution 2: Greater convenience, stronger emotional value

Over decades of urbanization, 600 to 900 million new urban residents have emerged in China’s lower-tier cities. Like middle-class consumers in top-tier cities, they use platforms such as WeChat, Xiaohongshu, and Douyin, gaining exposure to better brands and choices. However, local retail environments often limit convenient access to these products.

We have observed the rise of 10,000-store chain brands bringing higher-quality and newer products into these markets. Once labeled as “lower-tier,” we now view them as China’s mainstream consumer market.

In 2019, while visiting Changsha, we came across an intriguing store—Snack Is Busy. Its bright yellow storefront stood out, and inside a 100-square-meter space were dozens of categories and thousands of snack items, priced at 60–70% of supermarket levels. We quickly connected with the founder and became an early investor.

This combination of variety, convenience, and affordability has driven one of the fastest growth stories in China’s retail history. Within a few years, counties across China were filled with the brand’s yellow storefronts and red storefronts of Zhaoyiming Snacks. Today, its parent company operates nearly 25,000 stores nationwide. In January this year, Busy Ming Group was listed on the Hong Kong Stock Exchange.

Behind its low prices lies a restructuring of traditional distribution relationships. In conventional supermarket channels, brands must go through multiple layers of wholesalers, pay various listing and shelf fees, and endure payment cycles of up to 90 days. Markups across the chain often exceed 3x.

Busy Ming recognized early that by bypassing these intermediaries and purchasing directly from brands with cash, it could offer products at 70% of traditional prices. As volume increases, its purchasing and negotiating power strengthens, further accelerating growth through model innovation.

When we first met Mr.Yan, the founder, we asked whether this was simply a discount retail model. He replied: yes—but not entirely.

Perplexed, we asked for clarification. He explained: consumers do benefit from lower prices, but more importantly, they gain enjoyment.

For consumers in county-level markets, affordability matters, but equally important is a clean, well-lit shopping environment and the sense of freedom and enjoyment that comes with abundant snack choices. As he put it, “We are, in essence, a company that sells happiness.”

Subsequently, Jay Chou became the brand ambassador, familiar songs played in stores, and new flagship formats attracted widespread attention. Increasingly, it became clear that Busy Ming is not merely a snack retailer, but a provider of joy to young consumers across China.

The success of Busy Ming demonstrates another path of upgrading without price increases: enhancing convenience by penetrating vast lower-tier markets, while elevating emotional value by delivering abundance, ease, and enjoyment through “snack freedom.”

Beyond these approaches, the elements within the consumer value equation can be recombined to form new solutions. For example, Yuanji Dumplings achieves “performance + emotion” through better ingredients and freshly made products, building trust and expanding to 5,000 stores globally, bringing Chinese dumpling culture worldwide. Each consumer company can identify its own path based on its unique strengths.

Playbook: Enhancing two forms of value

Given the clarity of this approach, many entrepreneurs may assume it can be readily implemented. In reality, execution is far from straightforward.

Returning to the consumer value equation—performance, price, convenience, and emotion—these four elements can be grouped into two categories.

Performance and emotion fall under “user value,” determined largely by consumers. Businesses must deeply understand user needs and aspirations to succeed.

Price and convenience constitute “industry value,” driven by execution. Achieving affordability is not about compromising quality, but about innovating business models, shortening supply chains, and improving efficiency. Delivering ultimate convenience requires both digital channel mastery and extensive offline coverage across all market tiers—an undertaking that traditionally took decades to build.

To succeed today, companies must address both dimensions: First, focus on user value—performance and emotion—to answer what consumers want.

Second, build industry value—price and convenience—to answer how to deliver efficiently and affordably.

In practice, traditional and emerging companies each have distinct strengths and weaknesses.

Traditional companies possess deep capabilities in supply chains and distribution, yet often struggle with declining consumer affinity, with some brands perceived as outdated. The challenge is how to regain relevance.

A common misconception is that improving performance simply means better materials or more advanced technology. In reality, higher performance does not automatically translate into greater user value.

Last year, I visited a leading seasoning manufacturer specializing in sauerkraut fish. Despite strong investment in product quality and distribution, the company faced stagnating or declining sales.

I noted that while their seasoning may be superior, consumers ultimately want a ready-to-eat dish, not just ingredients. Many new brands now sell complete meal solutions online, achieving rapid scale within a few years.

Products that embed stronger user value stand out and become key profit drivers.

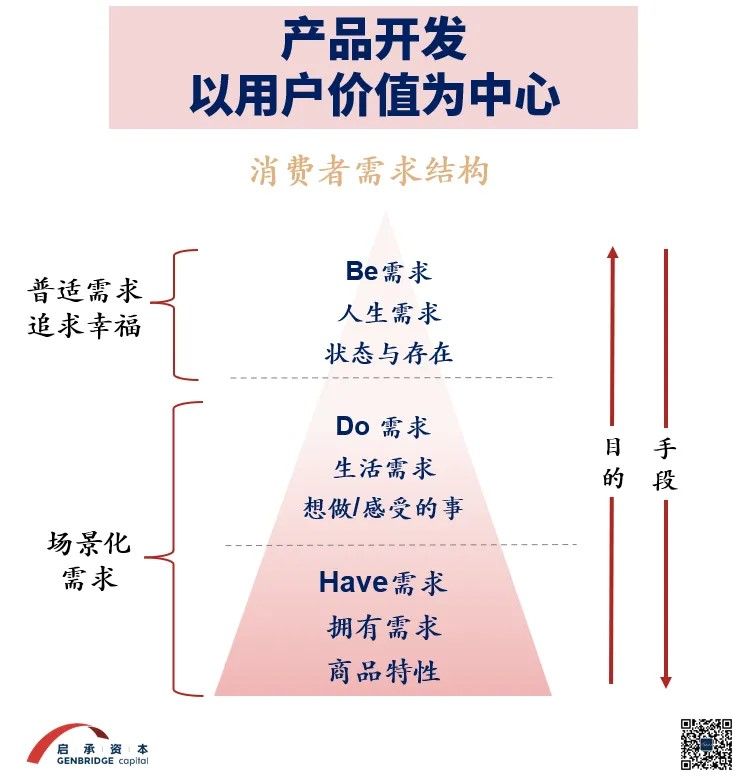

To better understand user value, we apply the “Have-Do-Be” framework, which helps systematically evaluate how products solve problems and shape user identity across scenarios.

For traditional companies, transformation begins with a shift in mindset—from focusing on “what we offer” to understanding “what users want, value, and aspire to be.” Those that achieve this shift are already entering new growth trajectories.

Turning to emerging companies:

Recent years have seen vibrant innovation, with new entrepreneurs leveraging emerging channels to scale rapidly. However, growth has not been linear.

In essence, new consumer brands follow a volatile growth curve:

They begin with strong product-market fit, enter a “valley of disappointment” amid competition, then refine capabilities and ultimately achieve a second growth curve through iteration.

In the long run, delivering high-quality products at low cost, ensuring consistency, and effectively reaching consumers across channels are all essential capabilities requiring sustained effort.

A story, toward a vision

I would conclude with a story.

Twenty years ago, I met an entrepreneur leading a 100-person team with RMB 100 million in revenue. When asked about his ambition, he replied: “To become China’s number one and one of the world’s top five retailers.”

An ambitious goal—how would it be achieved?

He said: “Consumer business comes down to three things: cost, efficiency, and user experience—relentless cost control, superior operational efficiency, and consistently exceeding user expectations.”

That entrepreneur was Richard Liu. Two decades later, JD.com has become one of China’s largest online retailers and among the world’s largest retail groups, built on these principles.

A decade ago, while working at JD.com, I witnessed the construction of world-class retail infrastructure by platforms such as JD, Alibaba, and Tencent. I believed this would give rise to a new generation of brands and offline chains—leading me to found GenBridge Capital.

Over the past decade, GenBridge Capital has partnered with more than 30 entrepreneurs to build brands deeply embedded in everyday life, from M Stand coffee to community retailers and dining brands increasingly present across China.

Today, I summarize our shared journey in one concept—“upgrading without price increases.” It is one of GenBridge Capital’s core insights into the evolving consumer landscape. We look forward to further dialogue and to developing new solutions that enhance everyday life for consumers.