China’s era of mass consumption has just begun

People tend to overestimate short-term changes while underestimating long-term trends. If one takes a longer-term perspective, the present moment actually serves as one of the best chances for making determined, long-term investments in consumer sector.

In the short term, economic fluctuations inevitably lead to weakened consumer sentiment, resulting in a decline in both consumption willingness and per-customer spending. However, from a long-term perspective, the rise of consumer sector in China is inevitable. Within the next decade, China is expected to become an economy where consumption contributes 70%–80% of GDP.

In the past, China's economy was driven by three main engines: foreign trade and then investment. However, by 2012–2013, investment had reached a low point, and with the mobile internet boom yet to take off, the economy was in a transitional phase.

In the past, China's economy was driven by three main engines: foreign trade and then investment. However, by 2012–2013, investment had reached a low point, and with the mobile internet boom yet to take off, the economy was in a transitional phase.

At that time, China's consumption was primarily business-driven rather than household-driven. For example, finding a four-person dining table in a restaurant was not common, whereas now, it is much harder to find a private dining room with a ten-person table.

Over the past decade, China has transitioned from an era dominated by non-household consumption to one centered on household consumption.

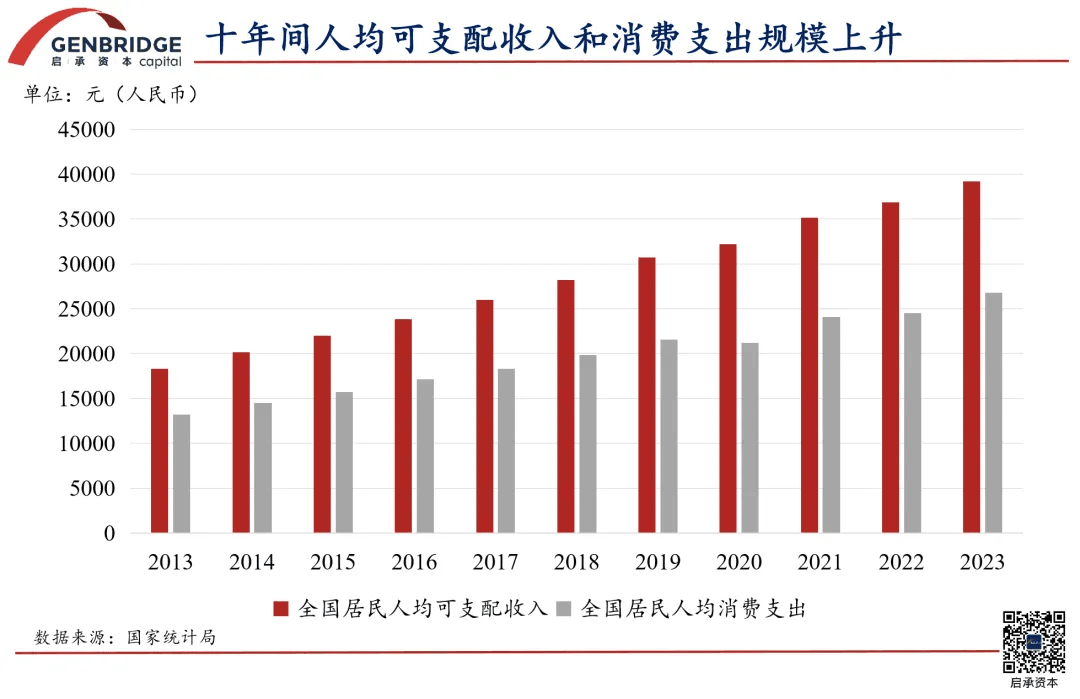

During this period, both household income and total consumption volume have increased. Additionally, with the explosive growth of the mobile internet since 2015, China experienced a wave of consumer upgrades in the saturation market from 2015 to 2019, during which many new consumer sectors thrived.

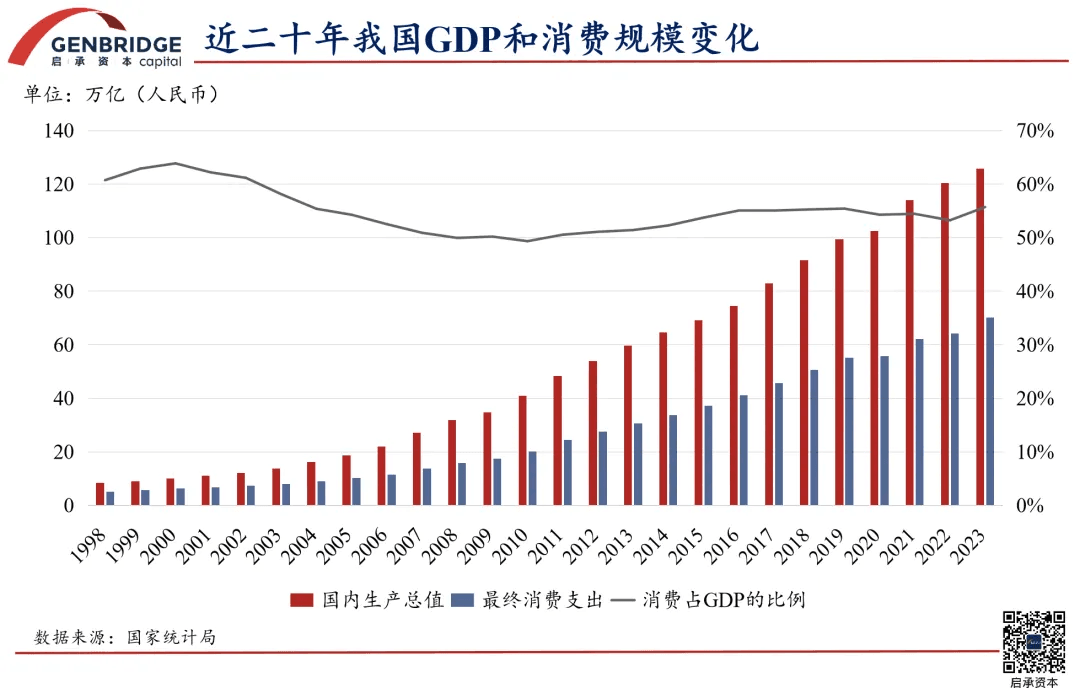

According to the latest data from 2023, China’s total GDP exceeded 126 trillion yuan, marking a 5.2% year-on-year increase. The total retail sales of consumer goods reached 47.14 trillion yuan, up 7.2% year-on-year, with consumption expenditure contributing 82.5% to economic growth.

Viewing current consumer industry through the lens of historical cycles reveals that even when the overall market is trending downward, there are still many structural opportunities within the market.

Viewing current consumer industry through the lens of historical cycles reveals that even when the overall market is trending downward, there are still many structural opportunities within the market.

For example, despite Yonghui’s large-scale store closures, GenBridge's portfolio, "Snack Is Busy" Group, has surpassed 10,000 stores this year and continues to experience rapid growth.

In this typical saturation market, where supply exceeds demand and consumer appetite remains relatively weak, the market landscape is undergoing rapid reshuffling.

Such structural transformations create significant opportunities, making this an ideal era for doing business. Even if 80% of players are struggling, the remaining 20% still have plenty of opportunities to make substantial profits.

How to locate a definite business?

In the realms of business and investment, people are always in pursuit of certainty, yet truly certain things are few and far between.

Looking at outstanding consumer companies, each has effectively addressed a particular social or life issue. It can be said that the scale of a business is directly proportional to the magnitude of the "problem" it can solve.

Take the US Tyson Food as an example; it not only produces chicken products but also expanded its business scope by acquiring beef companies. Its mission is to solve the global protein intake issue.

Thus, producing sufficient, high-quality protein product for all consumers is indeed a social problem that needs addressing. Tyson Foods even researches how to tackle greenhouse gas emissions from cattle farming to combat global warming.

These are fundamental, unchanging needs of humans beings. When a company recognizes social issues of this magnitude, its business potential becomes immensely imaginative—Tyson Foods, with nearly 90 years of history since its inception, continues to grow. The latest data shows its annual revenue exceeds $53 billion, with 140,000 employees.

To seek such certainty, GenBridge conducts cross-country comparative researches, observing how these predictable opportunities unfold and develop in different nations.

Take convenience stores as an example—consumer demand for ready-to-eat products, short-shelf-life items, high-quality protein, fresh food, and sugar-free beverages has been steadily increasing. This trend has already been repeatedly validated in Japan, Europe, and the US.

Once this certainty is identified, businesses must take practical steps to execute their strategies. In identifying business opportunities, three key factors come into play:

Internal Advantages

Opportunities often arise from change, and an entrepreneur’s sensitivity to these changes typically stems from deep industry connections and experience. This foundational insight enables them to turn opportunities into viable businesses.

It is crucial to monitor macro-level changes, such as urbanization, factory relocation, and shifts in community density, as these factors can significantly impact certain business models. Online platforms and big data analytics can provide valuable insights into the business opportunities hidden within these transformations.

Effective Positioning

In an evolving market, identifying a unique position is essential.

Take coffee as an example—Starbucks once held a dominant position in China. However, by analyzing the market segments, one can identify three distinct battlegrounds: dine-in coffee, takeaway coffee, and delivery coffee. Following the internet boom, Luckin Coffee capitalized on the delivery coffee segment, adopting a takeaway-plus-delivery business model to establish its niche successfully.

Differentiation Strategy

Once a market opportunity is identified, differentiation strategies can help businesses capture it effectively. Luckin Coffee’s store expansion strategy, for instance, involved opening delivery-focused locations near Starbucks stores. While these locations might not be as prominent, they offer lower rent and greater efficiency for quick deliveries.

Finally, as industries mature, many assume that opportunities dwindle. However, this is not the case.

In mature consumer markets such as Japan, the U.S., and Europe, a substantial number of M&A funds remain highly active. There are over 2,000 small-sized to mid-sized acquisition funds in the US, continuously driving growth and innovation in these so-called mature markets.

We believe that the greatest opportunities in saturation market arise from shifts in market share.

New choices in a new environment

At the same time, in a saturation consumer market, logic of doing business undergoes some changes.

In an incremental market, the prevailing logic is the entire industry experiencing takeoff. The early tea beverage market followed this pattern, allowing both top 10 brands to benefit from the overall industry's rapid growth.

In the current saturation market, the growth of tea beverage sector has slowed down, leading to intense competition. According to iiMedia Research, growth rate of China's freshly made tea beverage market would decline from 13.5% in 2023 to 5.7% in 2025. Yet, major brands continue to pursue scale aggressively—MIXUE has surpassed 30,000 stores, while Goodme, ChaPanda, and others are rapidly expanding toward 10,000-store targets. Even Heytea and Nayuki, which previously adhered to a direct-operated model, have opened up franchising to compete for market share.

This means that today, growth of any company within a category is essentially capturing market share from competitors. Company with the highest efficiency will secure the largest share.

Japan has witnessed this phenomenon multiple times in history. Brands like 7-Eleven, Uniqlo, and Nitori have all emerged over the past 20–30 years as efficiency-driven businesses. A similar trend is unfolding in China.

Some business models naturally hold an advantage in offline settings, often characterized by two key traits:

- Low per-customer spending

- High industry entry barriers

We believe that casual dining and community retail remain two sectors with massive growth potential.

Casual Dining

We categorize casual dining with a per-customer spending of under 100 yuan into two segments:

The first is "fast casual," with an average customer spending of 30 to 60 yuan, focusing on speed, particularly quick meal service.

Take Mi Village Rice Meal as an example. Although fundamentally a rice-based fast food chain, it differentiates itself by offering a dining experience with a casual dining feel. Consumers not only fulfill their basic need for a quick meal but also enjoy flavors distinct from home-cooked food, providing them with additional emotional value.

Despite its low per-customer spending and high profit margins, its profitability doesn’t come from cost-cutting but from maximizing store output—achieved through a high table turnover rate and efficient meal preparation. Typically, a turnover rate of 6–8 times per table per day is required for efficient operations.

The second category is "casual fast," exemplified by Chef Fei and Tai Er, which primarily differ from fast casual by focusing more on group dining scenarios, with an average customer spending of 60 to 80 yuan.

Casual fast food not only meets the needs of group dining but also offers shareable dishes, leading to a stronger willingness to pay among consumers. Compared to pure casual dining or formal meals, casual fast food still emphasizes efficiency, enhancing kitchen efficiency and sales contribution through signature large-portion dishes, thereby achieving quick cost recovery.

These two types of casual dining primarily seize new opportunities brought about by changes in consumer behavior. For instance, Mi Village Rice Meal and Chef Fei have store models that excel in profitability and returns, capable of recovering costs within a year and a half while maintaining high turnover and good profit margins.

Consumers are becoming more value-conscious, seeking high-quality, cost-effective solutions in recent years. Across various spending levels, they are actively looking for more affordable yet satisfying choices.

Community Retail

The retail industry is also worth paying close attention to. Compared to the restaurant industry, retail generally has a longer payback period, but it offers advantages such as lower fashion risks and cyclical risks, along with longer product life cycles.

For example, GenBridge Capital’s portfolios Snack Is Busy and New Joy, are standout players in the retail market. New Joy achieves a payback period of 18 to 24 months, making the relatively longer payback cycle in retail a reasonable trade-off.

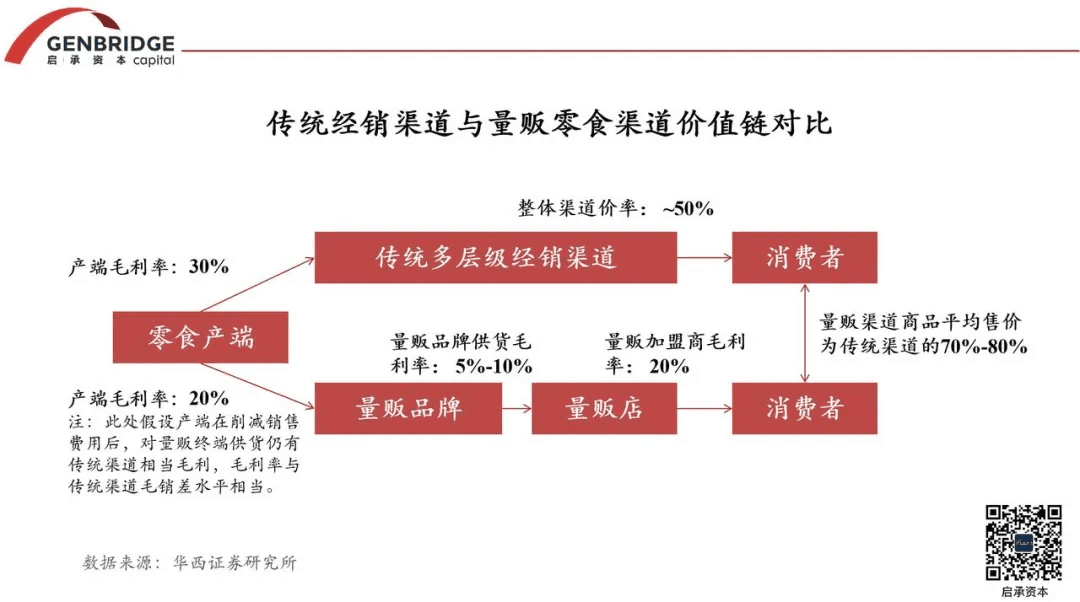

In China, snack purchases were historically dominated by online platforms and supermarkets, with supermarkets taking the lead. The supermarket model relies heavily on distributor-driven brand placement, often involving multiple distribution layers, which result in high markups throughout the supply chain.

However, the rise of brands like Snack Is Busy has disrupted this model. By lowering markup rates to 50-60% of supermarket prices and placing snack stores closer to consumers, these businesses have quickly won consumer favor and captured market share from traditional supermarkets—all while maintaining a diverse SKU selection.

As scale expands, efficiency improvements become a key opportunity in the snack chain industry. Through factory customization and private-label branding, snack chains enhance product quality while maintaining a high value-for-money appeal, increasing consumer purchase frequency.

The retail industry follows a relatively long lifecycle, consisting of a growth phase, maturity phase, and decline phase.

For example, in large supermarkets, the entire cycle spans approximately 25 years, with the growth phase lasting around 5 to 8 years.

When it comes to snack chain retail, China’s vast geography and the fundamental nature make the expansion process relatively long. Currently, the snack chain industry is in its seventh year of development, with an estimated one to two years of further network densification before it transitions into maturity.

During the maturity phase, leading companies will solidify their market positions through operational improvements and mergers & acquisitions. The merger of “Snack Is Busy” and “Zhao Yiming Snacks” led to the formation of China’s youngest 10,000-store retail chain group, securing a market-leading position even before the sector exits its growth phase.

Beyond snack chain retail, community retail—led by convenience stores—is another key focus area for GenBridge Capital.

The convenience store sector is often underestimated. Many believe that the market is highly competitive, that Japanese convenience store brands dominate, and that local brands struggle with profitability.

However, in terms of store count, convenience stores represent the largest category of small-format offline retail in China. They play a critical role in daily life, and despite intense competition, many domestic convenience store brands remain highly profitable. Franchised stores, in particular, can break even within approximately 18 months.

Investing in convenience stores requires relatively high capital, typically ranging from ¥800,000 to ¥1 million. To shorten the payback period, businesses must not only increase revenue and profitability but also reduce initial investment costs. In this regard, domestic convenience store brands have been highly efficient, optimizing investment costs to ¥500,000–¥600,000.

Conclusion

At this stage, market consolidation is an inevitable trend in industry development. This consolidation favors capable players who can continuously expand their market share through strong execution and strategic efforts. Companies can achieve market share growth either organically or through mergers & acquisitions.

The market undergoes constant changes throughout consolidation cycles. In consumer sector, there are rarely periods of absolute stagnation—new challengers will always emerge, injecting fresh energy and competition into the market.

GenBridge seeks to partner with outstanding enterprises in selected sectors, whether through minority equity investments or controlling stakes, working together to expand market share. Our goal is to ride the wave of market consolidation alongside our partners and achieve shared success.